Why Financial Advice Alone Doesn’t Change Behavior

The real reason you already know what to do — and still aren’t doing it

Most people reading this already know financial basics. Contribute to a 401(k). Build an emergency fund. Start investing early. Diversify. Spend time in the market instead of trying to time the market. Carry less debt than you think you need. Stop working when the math says the probability is high that you will not run out of money.

Most people are also not doing many of those things when they first come to see us.

That gap between knowing and doing is one of the most durable phenomena in personal finance, and in my experience, it is also the most misunderstood. We keep treating it as an information problem.

If people just understood the math, surely they would act. If they had a clear retirement timeline, surely they would follow it. If we showed them the compounding chart one more time, this time it would click.

But it does not click. It does not click because knowing and doing are governed by entirely different parts of who we are.

What Traditional Financial Advice Gets Wrong

Standard financial advice is almost entirely information based: “Here is what seven percent compounded over thirty years looks like. Here is the financial plan”.

You can hand someone a perfect plan and watch them not execute it. Not because they disagree with the math, but because something older and quieter is running a different program underneath.

Nowhere is this more visible than in retirement planning.

The standard retirement conversation is organized around doing. WHAT will you do with your time? Where will you travel? How much will you spend? These are the second questions.

The first question, the one that almost never gets asked, is this: WHO do you want to be with your time?

I have sat with clients who had every resource they needed to retire and could not do it, not because the numbers were wrong, but because they had no answer to the identity question. Work was not just what they did. It was who they were. The doing question had a ready answer. The being question was a blank page, and a blank page is terrifying.

Most financial advice never asks the being question. That is not a small gap. It is the whole game.

The Actual Obstacles: Identity and Inertia

Most of us didn’t sit down one day and consciously decide how we’d relate to money. We absorbed it. A parent who never paid full price for anything. A stretch of scarcity that made every dollar feel precious and every investment feel like a gamble. A first job that taught us, viscerally, that money only came from effort you could feel in your body at the end of the day.

Those early lessons didn’t stay in the past. They became the operating system.

Behavioral researchers have a name for the version of this that shows up in professional life: the doer identity. A sense of self built entirely around performance and output, forged in environments where doing was the currency of safety or approval. The pattern worked once — brilliantly, in fact. The problem is it keeps running long after the original conditions are gone, generating the very anxiety it was designed to prevent.

The financial version is everywhere once you know what to look for. The person who believes money only counts if she personally worked for every dollar of it. The business owner who cannot stop trading time for dollars even when his leverage has clearly shifted to capital and relationships. The saver who knows, intellectually, that holding two years of cash is costing her, but can’t shake the feeling that invested money is money she no longer controls. These aren’t bad decisions. They are identities. And identities don’t yield to spreadsheets.

The second obstacle is quieter, and in some ways harder to name. The people most caught by financial inertia aren’t irresponsible. They’re often the most responsible people in the room. They’re not making bad decisions. They’re making no decision — which feels safer, because inaction doesn’t feel like a choice. It feels like waiting for the right moment. It feels like being prudent.

Inertia wears responsibility's clothing very convincingly. And so you just drift.

What Actually Works

If it is not more information, and not a better spreadsheet, what shifts financial behavior?

It starts with different questions. Not what do you have, but what do you fear losing? Not what are your goals, but whose voice do you hear when you make a money decision, and what are they saying?

These questions do not replace the numbers. They make the numbers actionable. When a client can name the script she has been running, the script loses some of its grip. You cannot shed what you cannot see.

The second ingredient is pattern recognition from a professional outside your own story.

I have been in enough financial conversations to recognize the shape of an earner identity when I see it, to hear when a cash-hoarding pattern has crossed from prudent to costly, to notice when someone is describing a values conflict “dressed up” as a budget problem.

You cannot see your own blind spots. That is precisely what makes them blind spots. The right advisor is like a mirror that helps you see.

The third ingredient is accountability at exactly the moment you would otherwise stall. Not pressure. A hand on the shoulder at the fork in the road, the quiet question: are you pausing because you need more information, or because this is where the old pattern usually wins?

And the fourth, practically speaking, is making the first step small enough to take today. Not the full reallocation. Not the complete financial overhaul. One account opened. One meeting scheduled. One decision moved from the pending file to done.

Motivation is unreliable. Intentional action, even small, is what bridges the gap between knowing and doing.

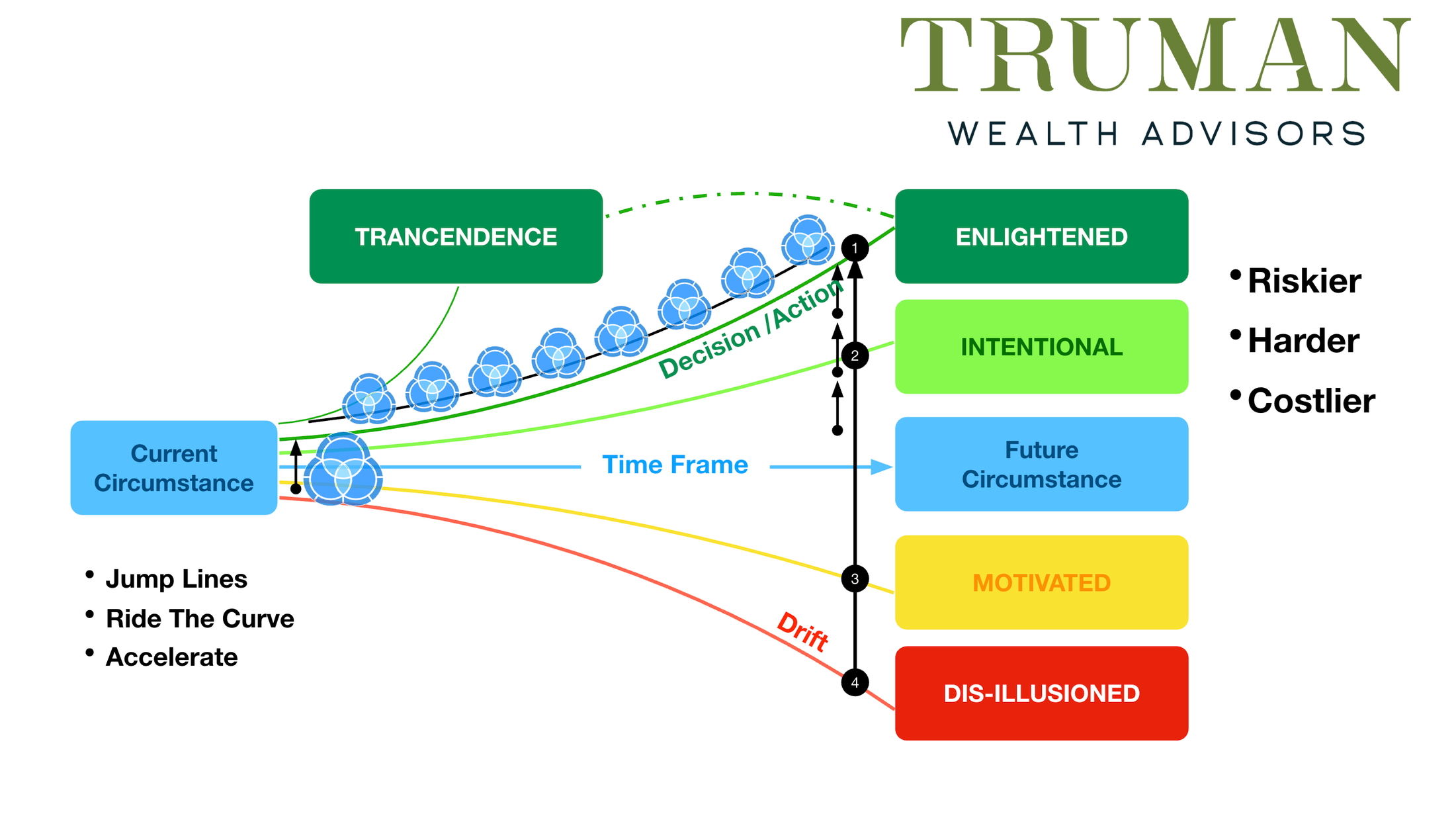

The chart below makes this concrete. On the left is your current circumstance. On the right, two radically different future circumstances, separated not by time alone but by a single fork in the road: Decision & Action or Drift.

And the chart labels the cost of waiting with uncomfortable precision: the longer you drift, the riskier, harder, and costlier it becomes to “jump the lines”.

Jumping lines is the concept I want you to sit with. It is the act of moving from whatever curve you are currently on to a higher one. Right now, today, the distance between the lines is the SMALLEST it will ever be.

The Work I Love Most

I became a financial planner because I believe that money was never supposed to be the obstacle. The TruWealth purpose, stated plainly, is to build a world where people have the confidence to thrive knowing money was never the obstacle. That line came from conviction, not from a marketing meeting.

But what I have learned from years of doing this work is that the real obstacle is rarely money itself. It is the story about money. The inertia that settles in when change feels harder than staying put. The script that has been running since before you were old enough to know you had one.

Delivering a plan is not the hard part of my job. Helping someone see what they could not see from inside their own story is. That is the conversation I find most meaningful, most rewarding, and most likely to actually move something.

If you read this and recognized yourself somewhere in it, I would genuinely love to talk. Not to hand you a spreadsheet. To start asking the questions that matter.

Reach out at mindy@trumanwealthadvisors.com or schedule directly at trumanwealthadvisors.com. The first conversation is always just a conversation.